Summary

- As Renzo seeks to optimize the depth and structure of liquidity for ezETH, Chaos Labs conducted a detailed analysis of key token user groups and developed a quantitative model to define liquidity requirements and appropriate price ranges. The primary objective is to ensure the protocol reliably supports user demand across diverse market conditions. This must be achieved while also improving capital efficiency and strengthening the overall resilience of the token and its holders.

- Chaos Labs analyzed behavior across key user groups, holders, arbitrageurs, loopers, and stablecoin borrowers, and built a model to determine liquidity needs and price ranges. We also evaluated DEX architectures to inform optimal liquidity shaping.

- We recommend providing 6,200 to 6,800 ETH of DEX exit liquidity, concentrated between the nominal ezETH/ETH exchange rate and a discount reflecting either instant withdrawal fees or exit queue yield loss. Deeper liquidity should sit closer to the nominal price to offer better-than-redemption execution. These recommendations aim to balance user experience with protocol sustainability and efficiency.

- Alltogether, we recommend having a total of 19,000 ETH-equivalent of total exit liquidity, inclusive of the DEX liquidity from the previous bullet point. This is meant to include both ETH and stETH, located either in a DEX or in the protocol’s liquidity buffer.

Overview and Requirements

The ezETH token

Overview of the token. ezETH is a yield-bearing liquid restaking token that is backed by ETH and its liquid staking derivatives, such as stETH. Due to incorporating both staking and restaking yield in its valuation, ezETH appreciates with time against the basket of tokens backing it. In contrast to stETH and several other LST & LRT, ezETH is not a rebasing token and does not need a wrapped version to be traded on most DEX.

Role of the DEX liquidity. For LRTs like ezETH, DEX liquidity establishes a secondary market, in addition to the primary market provided by the protocol’s mint and redeem functionality. In this aspect, they are very similar to LSTs like Lido’s stETH. Since these tokens are not traded on CEX, at least not in size, DEX liquidity should be sufficient to serve the needs of all ezETH user groups, providing an accessible and reliable alternative to the protocol’s liquidity pools.

Multichain considerations. While there is a significant presence of ezETH on Ethereum’s L2s, including Arbitrum (5.8k ezETH), Base (1.4k ezETH), Linea (16k ezETH) and Unichain (8k ezETH), the majority of its supply is on Ethereum. This makes user behavior on Ethereum more representative of the overall health and dynamics of the token. This analysis is chain agnostic where possible, but tailored to Ethereum otherwise. It can be seamlessly adapted to individual chains as user activity on those networks increases.

Objectives around DEX liquidity for ezETH

Deep DEX liquidity helps to achieve the following goals:

- By extending the liquidity beyond the primary markets, deep DEX liquidity reduces reliance on the protocol’s liquidity buffer, eventually enabling the protocol to operate more capital efficiently and sustainably over time.

- Ample DEX liquidity helps improve the trading experience for users who want to enter or exit ezETH positions by keeping the price impact close to the current market price and competitive with similar tokens. This encourages more active trading and cross-chain user engagement.

- While the mint/redeem mechanism is the primary driver of price stability, ample DEX liquidity facilitates smoother and faster recovery when ezETH trades below its peg by enabling arbitrage and market-making activities across venues and chains.

- DEX liquidity ensures smooth and efficient liquidations when ezETH is used as collateral, helping to prevent bad debt in lending markets. Liquidator bots must be able to sell sufficient amounts of ezETH without causing excessive price impact. Efficient DEX liquidity supports this process and ultimately drives greater adoption of ezETH on lending platforms, as well as expands its usage across the broader DeFi ecosystem.

- Relying solely on the protocol’s liquidity buffer can concentrate risk and create central points of failure. In contrast, DEX liquidity spreads market activity across numerous participants and venues, strengthening the overall system’s resilience and ultimately protecting ezETH holders.

Renzo’s Liquidity Buffer as an Alternative to DEX liquidity

In the past, the roles of the Renzo protocol’s liquidity buffer (LB) and DEXes were completely separated. The DEXes were external to the protocol, and functioned as a liquidity source for rapid exchanges between ezETH and other assets. They featured swap fees, collected by liquidity providers. In contrast, the liquidity buffer provided withdrawals without a fee, but not instantaneously.

However, that has now changed, as:

- Renzo is now offering an instant withdrawal option from the LB, for a fee collected by the protocol itself.

- Renzo has launched a Dynamo DEX, in which the swap fee is linked to the liquidity available in the protocol’s LB.

In addition, Renzo integrates solvers, who will use the LB directly for swaps. This will allow them to offer more competitive rates in intent-based DEXes, such as CoW Swap, and deeper liquidity when needed, for instance, for large liquidations.

The instant withdrawal fee is determined by two configuration parameters: minFeeBps and maxFeeBps, corresponding to the lower and upper bounds of the fee. Its exact value depends on the liquidity remaining in the LB after the requested withdrawal is completed.

The instant withdrawal feature has the benefit that all fees go to the protocol, in contrast to DEX trades, where fees are typically collected by third party DEX LPs and the DEX itself. However, at this point, we do not recommend fully replacing DEX liquidity with the mint/redeem mechanism. The reason is that DEX liquidity remains more tightly integrated with a multitude of DEX aggregators and liquidation bots. While the solver integration directly with the mint/redeem mechanism mitigates these concerns, the presence of alternative exit liquidity options gives a better safety margin and avoids a single point of failure.

User groups

Gaining deeper insight into these groups and their behavior helps us understand liquidity requirements not only in response to market events but also within the context of broader trends around token usage.

Holders

We use this term to describe protocol users who:

- Typically, do not engage in active trading

- May respond to incentive programs

- React slowly to individual market events, but are more sensitive to broader trends around ezETH and Renzo

Holders would use DEX liquidity when:

- Entering and exiting positions

- They are likely to require more exit liquidity when the market crashes (to get funds required elsewhere) or the market spikes (to take profits)

Arbitrageurs

We use this term to describe actors who buy ezETH at a discount and then redeem it. While other types of arbitrages between the DEX and the mint/redeem mechanism are possible, their share is insignificant for Renzo’s ezETH. (There’s also DEX/DEX arbitragers, but they aren’t considered to be protocol users in this analysis, since they are typically not exposed to ezETH.)

Arbitrageurs would use DEX liquidity when:

- DEX liquidity is overpriced or underpriced relative to the rate implied by the redemption mechanism:

- Either through the protocol fee, for instant redemptions

- Or through the yield lost due to waiting in the exit queue, for delayed redemptions

- It’s mispriced due to market events.

The figures below show that arbitrage activity has been relatively muted for ezETH. On average, only around 20% of all withdrawals are classified as arbitrage operations, and their share has decreased since March 2025.

Share of arbitrage redemptions vs. all daily redemptions:

Arbitrageurs help maintain DEX prices in line with the fair value established by the mint and burn mechanism. However, since DEX liquidity primarily serves other user groups with greater benefits, we do not recommend optimizing liquidity specifically to accommodate arbitrageurs.

Lending Protocol Loopers

We use this term to describe actors who borrow ETH-correlated assets against ezETH, usually to collect leveraged yield.

These users have no risk from the ezETH market price change. However, they are still responsive to ETH borrow rates. As a result, their liquidity demand is trend-driven, not reactive to short-term market events.

Loopers would use DEX liquidity when:

- Entering and (especially) unwinding their positions

- Unwinding positions are more likely to benefit from deep liquidity, as entering is instantaneous and costless using the minting mechanism.

- More likely to need liquidity when ETH borrow rates spike → Loop deleveraging is required

- Not at risk of liquidation unless at extreme leverage levels

This market is dominated by Aave, with mainly wstETH being borrowed against ezETH.

Stablecoin borrowers

We use this term to describe actors who borrow stablecoins against ezETH.

Typically, they do not use looping. While they may use a DEX to enter and exit their positions, they do not require a DEX or instant withdrawals, in contrast with the previous group.

Stablecoin borrowers would require DEX liquidity when:

- Indirectly, when at risk of liquidations from ezETH market price change.

- Liquidator bots must have sufficient exit liquidity for ezETH to sell the required amount of collateral, typically 50% to 100% of the total.

Borrowing stablecoins against ezETH collateral is dominated by Spark, which currently has a 40000 ezETH supply cap. Since there are only a few large positions, and they are not at risk of liquidation, we propose that the protocol set up alerts to react quickly in case that changes. If liquidation risk appears, we recommend a case-by-case approach.

As lending activity on Spark becomes more diverse, Chaos Labs is ready to provide estimates of the DEX liquidity required to support efficient liquidations using Monte Carlo simulations of at-risk positions, modeling price and borrow rate trajectories based on historical market stress periods.

DEX Liquidity Model

Actors

There are three main actors in the system:

- DEX traders. Buy and sell ezETH on a DEX.

- They either belong to one of the user groups described above or are automated bots that arbitrage between multiple DEX and liquidity pools.

- For the purposes of this model, we ignore the latter group of DEX arbitrage bots, since they do not hold the ezETH tokens for any significant duration and do not materially impact the outcomes of the other user groups.

- DEX liquidity providers (LP). Provide ezETH and ETH liquidity at a specific price range.

- LP have a specific reaction time. It can be:

- from seconds/minutes, for the more agile operators;

- to days or weeks, for instance, when range adjustments need governance approvals.

- Liquidity can be either privately owned or owned by the protocol itself.

- LP have a specific reaction time. It can be:

- Protocol team.

- Balance the protocol’s liquidity buffer size.

- Set parameters such as the instant withdrawals fee range and the minimal duration for delayed withdrawals.

- Incentivize liquidity provision and/or provide liquidity themselves via DAO treasury.

Defining the “Fair Price” Range

The protocol aims to keep the ezETH token supply steady or rising. Correct positioning of liquidity can help these goals. In contrast, when ezETH on DEX is underpriced:

- Users are disincentivized to mint new ezETH.

- Users are incentivized to redeem their existing ezETH.

This suggests that ezETH on DEX should be priced “fairly”, not just for the users but also because of the protocol’s self-interest.

As a general principle, we propose that most of the DEX liquidity is placed between the fair buy and fair sell prices, and propose the following thresholds for them:

-

For the fair buy price (upper limit), use the nominal ezETH/ETH exchange rate.

-

For the fair sell price (lower limit), use the nominal ezETH/ETH exchange rate minus the smaller of the two:

- The ezETH yield that’s predicted to be lost due to waiting in the exit queue.

- The current fee for instantaneously redeeming ezETH through the withdrawal contract.

The actual DEX price is expected to oscillate between the two limit prices, approaching the upper limit in periods where the demand for ezETH is positive, and the lower limit when the demand is negative.

The fair buy price is easy to determine, while the fair sell price requires knowing the waiting time and the expected yield. The average waiting time for withdrawals if queued up is approximately 6 days, as of May 2025. The yield can be predicted from historical data, giving relatively precise estimates.

Determining Fair Price of ezETH by Scenario

Let’s assume that the ezETH yield is 4.0% APR, minFeeBps set to 0.05%, maxFeeBps to 0.1%.

- The liquidity buffer is full, and the expected wait time is 6 days.

- The effective fee is 0.05%.

- Yield lost due to waiting is $6/365 \times 4.0= 0.066%$.

- The recommended lower bound of DEX liquidity is $\min{(0.05%, 0.066%)} = 0.05%$ below the nominal exchange price.

- Same expected wait time, but the liquidity buffer is nearly empty.

- The effective fee is 0.1%.

- Yield lost due to waiting remains 0.066%.

- Recommended DEX liquidity lower bound: $\min{(0.1%, 0.066%)} = 0.066%$.

- A crisis situation where the liquidity buffer is empty.

- Instant withdrawals are not possible.

- The waiting time is up to 14 days, which is required to go through the EigenLayer unstaking process.

- Yield lost due to waiting is $14/365 \times 4.0= 0.15%$.

- The recommended discount for the DEX liquidity lower bound is 0.15% or higher to account for the uncertainty of the situation.

The DEX price history of ezETH shows that it has been trading below the fair price. Since March 2025, this has corresponded to a higher implied lost yield of around 0.05% to 0.1%, occasionally up to 0.2%. The peak in mid-April is connected to incentives going live on Unichain, which created a large spike in ezETH demand.

The demand for ezETH can be quantified in two ways:

-

By looking at the difference between the amount minted and redeemed.

-

By looking at the difference between the amount bought and sold (to liquidity pools).

In the past, the mint/burn mechanism completely dominated the picture. However, since the start of May 2025 the demand has shifted to mostly being driven by DEX liquidity, the amount of ezETH bought daily by holders remains highly positive on average:

Over the past three months, ezETH on the DEX has decent liquidity, as most trades experience low price impact. Higher price impact trades occur but are relatively rare, indicating that larger trades may face more slippage but typical trades can happen with minimal cost. The reduction in price impact for ezETH purchases can be explained by temporary DEX liquidity oversupply, thanks to the LP incentives on Unichain.

Liquidity Shape Recommendations

Unless the DEX LPs can react instantaneously, it makes sense to provision liquidity for a range of fair sell price values, using the maxFeeBps value of instant withdrawals as a pessimistic lower bound.

Liquidity can be either flat throughout the range or (if possible) shaped to decrease linearly between minFeeBps and maxFeeBps.

In addition, to account for the situations when the liquidity buffer gets depleted, two approaches can be used:

- (If LP reaction time is fast enough.) Monitor the remaining size of the liquidity buffer and the associated instant withdrawal fee. When the fee reaches maxFeeBps for all withdrawals, shift the liquidity for a more pessimistic lower bound, corresponding to the number of days of lost yield expected at the current state, plus some markup for safety.

- (Otherwise.) Provide some liquidity from the maxFeeBps level to the discount level corresponding to 14 days of lost yield in order to enable trading and price discovery in this whole range.

Liquidity Shape: DEX-specific Considerations

There are currently two main DEX architectures of focus:

- Fluid: Concentrated liquidity in a single, anchored range.

- Uniswap-like: Concentrated liquidity in multiple, unanchored ranges.

Fluid enables automatic and costless liquidity rebalancing anchored to the nominal ezETH/ETH exchange rate from the protocol’s smart contracts. This pair’s current range on Fluid is between -0.3% and +0.0001% relative to the nominal exchange rate.

In contrast, Uniswap v3, its clones, and Uniswap v4 pools without hooks require manual rebalancing. On the other hand, Uniswap benefits from the option of having multiple liquidity ranges in the same pool. This enables more accurate liquidity shaping—avoiding over-provisioning at price points where minimal liquidity suffices, while also helping prevent the DEX from going completely out of range. The latter issue is particularly relevant for Fluid, since adjusting liquidity ranges in Fluid requires protocol parameter changes via governance.

Upcoming DEXes, such as Fluid v2, aim to offer the best of both worlds: automated, lossless rebalancing and support for multiple ranges. This is also achievable through Uniswap v4 pools with hook and external oracle integrations.

Renzo has recently launched Dynamo DEX on Unichain, which features a dynamic fee hook. While a good first step, this design could be further improved by shifting the liquidity dynamically, particularly by anchoring the liquidity to the nominal price.

DEX Liquidity Recommendations

Approach

In order to estimate the DEX liquidity required, we focus on the needs of the holders. This includes both holders of the ezETH token, as well as the Aave ezETH collateral token, which is a form of exposure to ezETH. The second token covers the “lending protocol loopers” user group.

The approach to determining the required liquidity focuses on the exit liquidity (denoted in ETH). The amount of ezETH liquidity on DEX is less important, as users should be encouraged to mint new ezETH in demand periods rather than buy it.

The main idea is that the DEX liquidity should cover the holders’ needs in most situations, reducing the pressure on the protocol’s exit queue.

Changes in the holders’ exposure to ezETH include these events:

- Mints and redemptions of ezETH

- It does not include mints/redemptions for Aave ezETH since it does not change the exposure to the underlying asset.

- Transfers of ezETH and Aave ezETH to non-holder addresses

- These include sales of ezETH to liquidity pools.

The period covered is from January 1 to June 16, 2025. This includes multiple market stress events, with a drawdown in ETH price from $3600 to $1400 from January to April.

Results

These results are averaged over a 14-day window and presented cumulatively for all holders. The 14 day window length is selected as that is the unstaking duration from Eigenlayer’s contracts.

Absolute change in ezETH held, daily:

Relative change in ezETH held, daily:

99-th percentile worst results:

- Relative change of −0.75% per day

- Absolute change of −466 ezETH per day

95-th percentile worst results:

- Relative change of −0.67% per day

- Absolute change of −419 ezETH per day

Multiplying these results with 14 (days) and 1.05 (the current ezETH/ETH exchange rate) we see that these results suggest 6.2k to 6.8k ETH exit liquidity, sufficient for the whole 14-day unstaking period.

Validation using stETH. Since ezETH only became redeemable in July 2024 and was listed as collateral on Aave in October 2024, we use data from the more mature asset—Lido’s stETH—to validate the model.

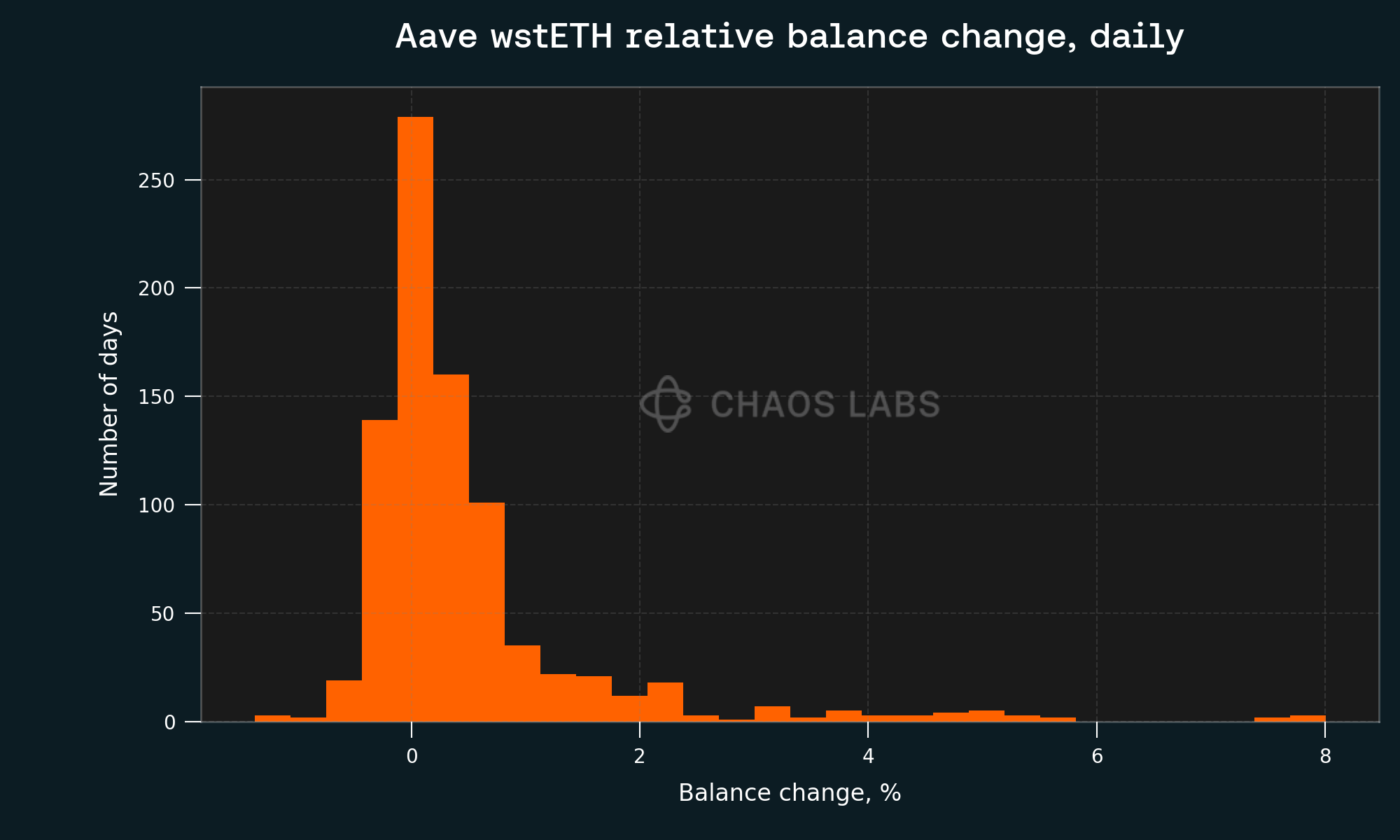

The plot below shows Aave’s wstETH collateral (main market) token balances over time:

We look at the negative changes in this token’s balance to detect deleveraging events. The relative change is of the main interest, since the absolute supply of Aave wstETH is much higher than of ezETH:

The results are, for the worst 99-th percentile:

- Relative change of −0.69% per day

95-th percentile worst results:

- Relative change of −0.35% per day

We repeated this analysis above for the overall balance changes of the stETH token supply. The period of analysis was January 2022 to June 2025, and we specifically excluded stETH and wstETH in liquidity pools. This gives even lower daily change values (P99 = −0.21%, P95 = −0.12%).

Taken together, these results validate the estimates obtained from the ezETH token.

Total Exit Liquidity Recommendations

We recommend that most of the 6,200 to 6,800 ETH exit liquidity be placed in DEX outside of the protocol’s Liquidity Buffer. This is due to the reasons discussed in the “Protocol’s Liquidity Buffer” section.

In addition to this DEX amount, we recommend a significant exit liquidity in the LB itself, selected using more conservative assumptions. This is necessary as the LB functions as the key driver of ezETH’s peg stability. In addition, keeping the exit liquidity in the buffer is less expensive than keeping it on a DEX.

As a result, we propose the following methodology to model the total exit liquidity (DEX + LB):

- Instead of directly tracking the historical outflows, track the percentage of ezETH holders redeeming in period of time, and consider the redemption activity during a time of market stress.

- Instead of looking at the historical net balance changes (minted amount minus the redeemed amounts), assume that no new ezETH was minted in the 14-day period. This worst-case assumption models a risk-on period with no demand for the asset.

- Perform a Monte Carlo simulation of holder redemption decisions using the historical redemption probability and the historical average % of holdings redeemed.

The figure below shows the results. Applying this methodology gives liquidity requirements between 15,000 and 20,000 ETH as the 98th percentile risk level, depending on the redemption frequency.

Using the medium-conservative value of 0.015 of ezETH holders redeeming per hour, the model gives 19,000 of total ETH exit liquidity. This can be denominated either in ETH itself or stETH, since the protocol both permits redemptions in stETH and stETH itself is more easily redeemable to ETH, as it does not have to go through the Eigenlayer’s 14-day waiting period.

For example, if the protocol decides to go with 6,500 ETH as DEX exit liquidity, then we recommend the following allocation:

- 6,500 ETH total in DEX such as Fluid and Uniswap, distributed between the Ethereum mainnet and Unichain.

- 12,500 ETH-equivalent in the liquidity buffer (excluding finalized-but-unclaimed withdrawals), most of that in the form of stETH.

Current Liquidity Breakdown: Liquidity Buffer and DEX Exit Liquidity

During the past months, the Renzo liquidity buffer oscillates between 25k and 30k ETH-equivalent, with the majority of assets denominated in stETH. This composition is cost-efficient and consistent with the protocol’s goal of preserving capital while ensuring redemption capability, especially during high-stress periods. The ETH share in the buffer has shown some variability but generally remains above 5k ETH. The liquidity buffer currently holds more than double the 12,500 ETH-equivalent minimum recommended in the report. This provides a significant safety margin, even for risk scenarios that were not explicitly modeled. In the case of solvers being successfully integrated, the buffer may prove more than sufficient, and the protocol could consider reducing its size to improve capital efficiency.

Liquidty

The total DEX exit liquidity currently stands at over 8k ETH, with over 60% concentrated on Unichain, driven primarily by recent incentive programs. Ethereum mainnet currently holds only ~2.5k ETH, with a large share deployed on Fluid. While the total figures are in line with our recommendations, the concentration and accessibility of the liquidity across chains introduce important considerations that warrant further analysis.

Scope and Limitations of this Model

This model is designed to be suitable for both calm and volatile markets; however, some situations fall outside of its scope:

- ezETH redemptions are paused. Since time-to-redeem is a model parameter, it cannot give accurate predictions if this duration is unknown.

- ezETH minting is either paused or capped. Either of these could push the fair price of ezETH above the nominal exchange price, necessitating the addition of DEX liquidity in the range that is currently not considered.

- A black-swan mass liquidation event. Renzo’s smart contracts have a pause mode that will be activated in case suspicion of a mass slashing on the Beacon chain, significant slashing on Eigenlayer’s AVSs, or a similar black-swan event occurs. This ensures that mass liquidations for users looping ETH against ezETH do not happen even under these conditions. For stablecoin borrowers, since there are no lending protocol positions potentially at risk of liquidation, we propose that the protocol keep monitoring the situation and add DEX liquidity on a case-by-case basis to cover each risky position whenever such arises. It is also important to ensure that liquidation bots can use the liquidity buffer directly, through the instant withdrawal feature; the protocol should either run its own bots or help existing bot operators to integrate this liquidity source.

Recommendations and Outlook

Our main recommendations are:

- Provide 6,200 to 6,800 ETH of DEX exit liquidity to cover the exit needs of holders.

- Place the DEX liquidity between the nominal ezETH/ETH exchange rate and the discount corresponding to the maxFeeBps parameter of the redemption contract.

- If possible, place deeper liquidity closer to the nominal exchange rate, particularly in the region between the nominal exchange rate and the minFeeBps discount, so that DEX sales offer a better price than the redemption mechanism.

- While setting the minFeeBps and maxFeeBps parameters is not in the scope of this article, we assume that they are set to approximately correspond to the yield lost due to waiting in the unstaking queue.

- Support that with a substantial ETH-equivalent liquidity in the protocol’s liquidity buffer, in accordance with the integration of solvers, which is expected to reduce reliance on external DEX liquidity over time.

As the next steps, Chaos Labs is ready to provide its recommendations on the best ways to create the desired shape and depth of liquidity. We see high potential in utilizing Uniswap v4 hooks to make LRT liquidity provisioning more self-sustainable and to target the incentives where and when they are needed the most.